From innovation to infrastructure: CDR in APAC

Last week I had the privilege of opening Puro.earth’s 2026 APAC CDR Forum in Singapore.

The title of my keynote was “From innovation to infrastructure.” It is a phrase we have been sitting with for a while, and here I want to unpack what it means, and share what the data is telling us about durable carbon removal in the Asia-Pacific region.

Are we done with innovation?

I started the keynote with a deliberately provocative question: if we are pivoting to infrastructure, does that mean the innovation chapter is closed?

It is not. The two things are happening in parallel, and we need both.

The first is innovation within the pathways we already know. There is enormous room left to improve how biochar, enhanced rock weathering, terrestrial storage of biomass, and bioenergy with carbon capture are produced and integrated. Industrial integration, efficiency gains, new feedstocks, new supporting infrastructure – these are not minor refinements. They are how unit economics get to where they need to be.

The second is entirely new pathways. Oceans, minerals, microbes, novel products. We have not figured out every way to draw CO₂ out of the atmosphere. The next category-defining pathway probably exists today in someone’s lab or pilot facility.

What changes with “infrastructure” is not the appetite for innovation. It is the recognition that for the methods that work, we now need institutional-grade market infrastructure – registries, standards, contracts, financing – that can carry tonnes at scale, year after year, while also standing up to the expectations placed on it in terms of integrity, due diligence and rigour by institutional buyers.

APAC: an early start, and a strong 2025

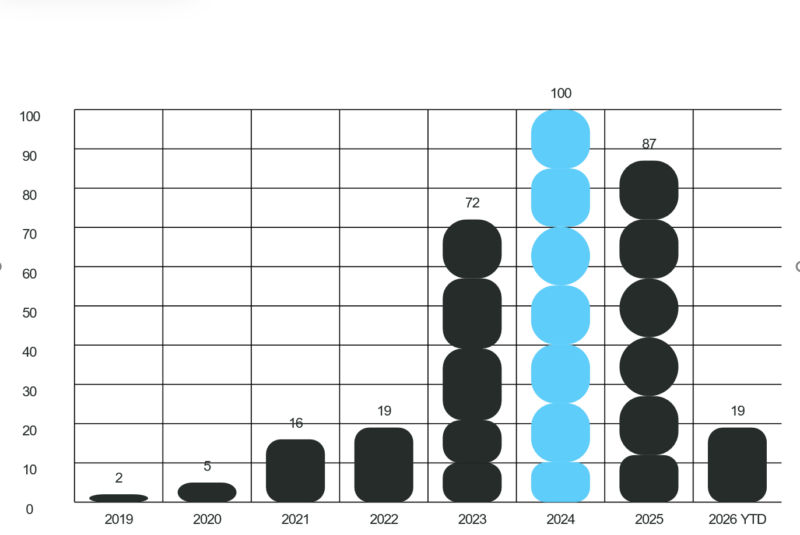

Puro.earth’s APAC story began earlier than most people remember. Two Australian suppliers signed our Platform Agreement back in 2019, and from there we saw a fairly clean exponential growth curve in supplier registrations through 2024.

2025 was a difficult year to raise money for many of the new CDR project developers, which gave us a feeling that it would in turn be a challenging year. However I was genuinely pleased when 87 APAC suppliers signed up over the course of last year. That is a strong vote of confidence, and we expect that the next few years of issuance in APAC will closely follow the growth in our regional supplier base.

New APAC suppliers signed-up to Puro.earth

A regional map that has been redrawn

The single most striking shift I want to flag: at last year’s count, China had two registered suppliers on the Puro Standard. Today it has 13. That is the kind of jump that gets your attention.

Across the region, the spread now looks like this: Australia (23), China (13), India (12), Singapore (11), Thailand (4), with meaningful presences in Indonesia, Japan, Malaysia, Cambodia, Hong Kong, New Zealand, Taiwan, and Vietnam. APAC suppliers now make up roughly a quarter of all registered suppliers globally.

What is actually being produced

Biochar continues to dominate APAC issuance, and this matches the global picture – biochar has been the backbone of durable CDR delivery for the last several years. But the methodology mix is starting to diversify in ways that map to regional resource bases.

Enhanced rock weathering has real potential in India over the next few years. Terrestrial storage of biomass works in dry climates such as much of Australia. Each pathway finds its geography. APAC’s strength is that the geography is large enough to support several.

Demand is finally moving

Retirements are where I see the most encouraging change. CORC retirements by APAC-based buyers jumped by an order of magnitude from 2024 to 2025, and 2026 is shaping up to continue with growth. This matters because it is the leading indicator that demand from APAC corporations is moving from interest to procurement.

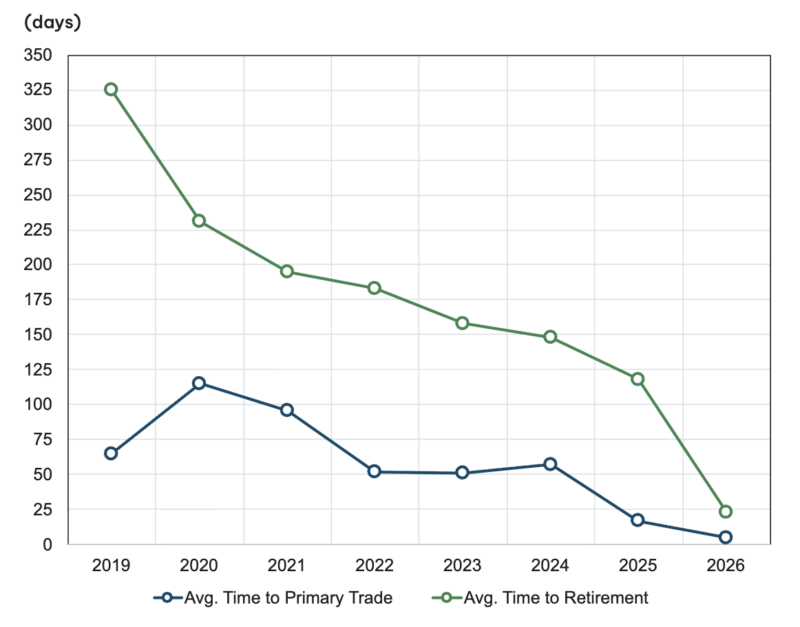

Speed matters as much as volume

We track two operational metrics closely. How long does it take to get credits issued, and how long does it take for issued credits to be sold for the first time?

We have invested heavily in efficiency here, which supports time to revenue for our suppliers. The number I am proudest of: in 95% of cases, we issue credits the next business day after receiving the auditor’s report after an output audit.

Time to primary trade after issuance has also come down considerably, which means corporate buyers are queuing up to purchase, rather than the credits sitting on the shelf – meaning suppliers are also getting paid quickly.

The fact that retirements happen quickly after the credits are transferred replenishes the demand signal for the next cohort of supply.

The market share trajectory

Looking at supply share within our ecosystem: in 2025, CORCs issued by APAC suppliers sat at roughly 1% of all global Puro issuance. This year, we expect a roughly 12x increase in APAC volume in 2026, taking the regional share to around 8%. APAC is growing faster than any other region right now.

Other regions are of course growing too, and we do not expect APAC to break 10% of global share before 2028. The upside case – where APAC issuance moves faster than this – depends largely on whether ERW in India scales as projected, and whether Indonesia begins to convert its considerable biomass resource base into registered supply.

The infrastructure piece

When we say infrastructure, we mean the things that allow durable CDR to function as an investment-grade asset class. For Puro that means several things, working together.

One CORC represents one tonne of CO₂ removed, defined to a scientific standard, with a 100-year minimum contractual storage commitment. Buyers are not procuring an offset. They are procuring a defined, traceable, retirement-tracked asset that meets the due diligence requirements of banks and infrastructure funds.

Puro’s standing within the emerging policy architecture matters here. We are an ICVCM Eligible Carbon Crediting Programme, aligned with the EU Carbon Removal and Carbon Farming (CRCF) Regulation Framework, and operating within Article 6-compatible governance. These are not badges. They are the rails along which the next phase of carbon markets will run.

And Nasdaq’s backing of Puro provides something that is hard to replicate: the institutional weight, the transactional capability, and the insolvency protection that come with sitting inside a global exchange corporation. For suppliers building project infrastructure with 20-year horizons, and for buyers signing multi-year offtakes, that institutional grounding is what makes the commitment financeable.

Where we go from here

APAC has the suppliers. It has a credible pathway mix. It has rising domestic demand and increasingly serious policy signals: Japan’s GX-ETS going mandatory, Singapore’s carbon tax climbing toward SGD 50-80 by 2030, Indonesia working through its national biochar and CCS frameworks.

The structural gap is not supply readiness. It is coordinated institutional demand and the procurement frameworks that turn latent buyer interest into contracted tonnes. That is the work in front of us and it is the work that infrastructure, properly built, exists to support.

Thank you to everyone who joined us in Singapore. The conversations there confirmed what the data is showing: the region is ready for what comes next.

Highlighted photos of the event

Join our community of climate pioneers

Join our community of climate leaders

Receive updates from Puro.earth, along with CDR market updates and intelligence. By subscribing, you agree to Puro.earth’s privacy policy.